Like many others of my generation, I too lust over real estate, watch flipping shows, troll listing apps, and gag over mid-century modern homes that remain elusively out of my current financial reality. ESPECIALLY from my concrete NYC life.

Next thing I know, I’m texting tempting words like “Look this could be your studio” to my babe and thinking “Alls we need is a water source and a corner to grow food” and BOOM suddenly in my mind my besties and I are gonna survive the apocalypse and maybe even build financial stability in the meantime. If you feel me – read on below! And if you like this content, you might also enjoy:

- the Money Tips to Buy a Home instant-access digital workshop

- this MEGA post on the Whys, Surprises and Ethics of buying a home

So you want to buy a house with other people?

Yes! I get it: built-in community plus more people to pay in and more hands for the work plus all the house-owning benefits wrapped together.

Woop! What could possibly be complex?

Ahem. As excellent as that all is, the process of acquiring a property is NOT less work because you have more people working towards it. Let me speak from experience doing it, and helping others do it.

This post aims to help you know what to expect when you’re planning to buy property with others in a US context. This is at minimum a multi-month project. Run it like a marathon and remember to have fun!

This information is customized for those who are working on the dream of a property purchase with others to whom you aren’t married. If you are buying solo or with a wedded spouse, a lot of this info will be useful. Some of it will be excessive due to the complexities oh I mean joys of the current systems at play which automatically simplify ownership for you.

Ready? Get off your zillow / trulia / redfin for a bit and read this!

Part 1: acquire people and money, then house.

SECTION A: SET EXPECTATIONS & FIGURE YOUR PLAN

Step 1 – identify friend(s) you trust who will at minimum do basic paperwork, show up for plans and meetings, and dialogue respectfully with you. If you do not have such friends, DO NOT BUY A HOUSE WITH THEM. If you are not that kind of friend, also don’t. If you do have such friend(s), get ready to put them on speed dial because you’ll be starting with a conversation and then having many, many more.

Big why: what are your shared goals? Live there? Always or sometimes? Rent it out?

Big what: Is there a minimum number of bedrooms, bathrooms, or acerage you need? Garage? It needs to be one-floor and accessible? Make a list of must-haves and want to haves. This’ll help you understand the cost range of what you are looking for.

Big how: who’s got what down payment money? Who has a job and might be willing to explore getting the mortgage? Details will be figured out in upcoming steps, for now talk about the high level.

Step 2 – identify a general idea of where you and friends might buy house. Where you all live? Maybe. If you’re in an expensive city, or if you want a well or whatever on your compound then identify a plan B. Where might require some creative thinking. It will definitely depend on the numbers.

For example, if you’re a new yorker, you might wax poetic about “Upstate” and be looking at cute places for $250k or so. If you live in LA you might fantasize about Joshua Tree and think back to five years ago when livable cabins were $60k. The past is over, so you’ll need to plan to buy a $150k or up desert compound. If you’re living in Seattle start scraping up those dollars because you’re looking at $600k and up in most areas.

Note: To buy with a mortgage, there has to be something of value that is mortgageable on the property, usually a building. If the spot you’re looking at is just land, or only “improved land” but doesn’t have a structure, you’ll need to buy it outright in cash.

Step 3 – Get some REAL numbers (not just the ones that real estate apps try to seduce you with). You’ll need to know:

3a: What’s a realistic house/apartment/cabin compound SELL for (not list for). You’ll find this by looking at recently sold houses in the area(s) you’re looking at.

For example, sometimes (before 2021) places sell for $220k when the asking price is $250k. OK!

More recently, places sell for $650k when asking is $590. Otttaaayyyy. You gotta KNOW what you’re dealing with.

3b: From the sells-for information, what’s a down payment of 5%, 10%, 15%, 20% and 30%? This range is because you need:

- 3.5 – 5% for a house or multifamily (up to 4 units) you’ll live in as a primary residence

- 10% for a second home / vacation property single family

- 15% for a second / vacation multifamily

- 20% for a single family house you don’t plan to live in and will rent

- 30% for a multifamily you won’t live in and will rent

Note: you will pay an extra mortgage insurance cost, PMI, if you put down less than 20% in any case.

For example, For this $220k compound, we’d need to get a down payment of $11k @ 5%, $22k @ 10% — and $44k @ 20% if we’re buying it as a rental.

The more money you put down the lower your monthly costs AND overall costs in the long term. But, if what you got is 5% and a dream – you CAN move forward – well, except you have to cover closing costs…

3c: Learn about what closing costs are in the area you want to buy in? In most places you can assume you’ll need about 3-6% of the property cost to cover closing … except NYC, where there are extra lawyers needed, so estimate around 7-8%. This is money you “lose” – that is, it doesn’t go into the “equity” – the value of money paid into the place. Be prepared to say goodbye to that money.

Closing costs are everything from: loan origination fees, insurance and tax prepayments, title writing, transfer, and filing fees, and allll kinds of other stuff. They’re not optional. A good realtor will be able to give you reliable estimates.

For example, For my $220k compound, I’d need another $11k @ 5%. Ok, $22k minimum to do this, and up to $55k if I wanted to put 20% down to avoid PMI, and pay closing costs.

3d: Don’t forget that the mortgage is just the beginning. Don’t set yourself up to buy more house than you can pay for! It’s not 2007 and you are not going to make that mistake. Along with your mortgage (principal and interest) and your taxes and insurance, you’ll also need to pay for utilities, to maintain the place (assume at least 1% of house value/year), and oh like furniture and food for when you’re there.

DO NOT plan to spend every last dollar to acquire this property, and do NOT plan to max your spending on just the mortgage payment. That will not make a sustainable plan!

Step 4 – Get real: Who can get a mortgage for what house loan amount? You need demonsrateble income to get a mortgage, and usually a job that pays at least $50k (this can be hacked if your crew can pay cash for the property or can put down a bigger down payment).

The bigger the cost of the house, the higher the income needed to support it.

Six months out pro tip 1: Generally, you can get a mortgage that has a payment equal to around 30% of your total income, after any monthly expenses, like debts. So pay down debts as much as possible to qualify for more mortgage.

Six months out pro tip 2: Additionally, you could get a lower mortgage interest rate if your credit is higher – do NOT close credit cards when you’re trying to get a mortgage. Just pay your bills on time, pull your credit report and if there’s anything on your credit report you think you can clean up before you go try to get a mortgage, get on it.

Friend(s) who are not getting the mortgage – here is an opportunity to support by doing things like: helping the other person make and stick to a debt paydown plan or offering to follow up on credit report stuff.

HACK: if you usually write off lots of things because you have a side hustle, write off less in the year or two before you buy, so you qualify for a bigger mortgage (though obviously don’t take on more mortgage than you can reasonably pay for). You can always re-file with your expenses added back in after you’ve bought the place – and get a tax refund 🙂

Step 5 – Figure out where the money is coming from and where is it going.

5a. Who has money to cover down payment and closing costs, and where is it coming from? This is where the conversation gets real.

You do NOT need to each come to the table with the exact same amount of money. You DO need to be honest and transparent about where your money is coming from to avoid awkwardness and resentment. You DO need to make sure that someone isn’t going without to participate while others are still engaging in consumer spending willy nilly. This is

5b. Open a joint account. You’re gonna need it to pay for crap anyway. Unless someone can NOT be on a bank account for some reason, put all involved on the account. Put some money into this account to pay for things like inspections on houses you are considering buying and whiskey/champagne for when something falls through or comes through.

Why? For one, whomever is on the mortgage will need it to look like the money is theirs, as mortgagers are looking out for situations where someone gets backdoor loans for down payments and then has to pay them back and cant afford the mortgage. The mortgaging bank will want to look at the last 60 days of your account statements. If you’re scraping money together, put down payment funds in the paying persons’ account at LEAST two months ahead of time _or open and fund a joint account_ .

Technically if one person can float all the money, you can let them pay from their account and everyone can pay them back afterwards. But, my pro tip is: spend all your costs for this house project out of one account, on which all participants are on, for max tracking simplicity down the line.

NOTE: It’s neither income not illegal to send someone money, though amounts sent over $10k can trigger flags at the bank, and amounts over $15k can triggers IRS questions. You’ll have acceptable answers to these possible queries, but wouldn’t you rather avoid the possibility and just use a joint account? Yup.

Exercise: At this point, it’s wise to run some long term realistic numbers.

Try this calculator – see what it looks like if you pay extra on your mortgage or go for a place in a lower tax area, for example. Paying an extra month’s mortgage a year starting now will usually cut about five years off your payment clock – and interest payments!

Still realistic? Great – now you’re ready to REALLY play ball.

SECTION B: Once you are DAMN SERIOUS

Step 6 – Find a realtor. You’re ready – go find someone recommended in the area you’re looking in. Get their estimates on closing costs and sales prices versus listing prices and refine your estimate on what you can afford to buy given their expert opinions. This person is your champ so treat them like gold. Also, you need to like their style because you will be communicating a LOT.

Step 7 – Prequalify for a mortgage, ideally using a broker your realtor recommends but feel free to shop around. A “prequal” is less paperwork than a mortgage, but it signals you’re serious (and can pay) to a seller. Depending on your market, you might need to get preapproved – a lengthier process. Either way, you’ll only get an estimate of the interest rate you’ll ultimately get once you actually go into a mortgage.

Person on the mortgage > Get your last two years of taxes together, bank account and savings account and retirement statements. They’ll want to see where the down payment is and that it’s not every last dollar you have. They’ll want to see that you’re employed regularly. If you’re a full-time freelancer, pull up all your invoices for the last two years and get ready for a long conversation.

Person(s) not on the mortgage > be helpful to person gathering all that paperwork because it’s a pain in the butt. Make them dinner? Offer to create a folder or filing system to help, or be on email duty.

Step 8 – Think and talk about the end at the beginning. It sucks, but one of you will probably die first. Before then, one of you might want to step out of the arrangement. You do not need to plan everything about how might you handle that before you buy with someone else, but don’t skip this convo for two reasons:

8a. No surprises are the best surprises when they might cost you thousands of dollars or a friendship.

8b. Plan how you’ll do the paperwork. While only the person who looks best on paper can go on the mortgage, all of you can usually go on the deed. The deed indicates ownership (and the bank is also on it if you have a mortgage), so How you’ve set up legal ownership of the place will impact how someone can step out and what happens when someone dies.

Your ownership structures are limited by laws, which differ by state and are set to favor solo or married couple ownership, especially when it comes to transfer of ownership upon death. Womp womp. The LAST thing you want is for someone to die, their evil family to drag their portion of the property through court, and the rest of you have to deal with that while grieving. Don’t do that. Plan to make Wills AND set up the ownership of your house right (which’ll save you $1k not having to re-do it!)

Look into whether you’re in a Community Property state or need to discuss Joint Ownership (each owner owns a segment, which they can bestow to someone else upon death) vs Joint Ownership with right of Survivorship (ownership transfers to surviving owners upon death). Also this is not legal estate advice so DO double check it for your specific location!!

Step 9 – Go house hunt! I highly recommend taking your must-have and want-to-have list and making a form you can fill out for every place you see, adding in fields for condition, notes, location and flags. This will both jolt memory and make the situation of having to compare places to decide which to put an offer on much easier.

Pro tip: unless someone is about to come up with a secret stash of money, or is willing to ask a parent for extra funds, there’s little point in you going to see houses you know you can’t afford UNLESS there is a good reason to believe you can put in a low offer and not need to magically find more money. That’s a convo with your realtor.

Step 10 – Put in an offer! Work with your Agent to come up with a starting number and a strategy.

For example, The place we like best is $320k but it’s been on the market awhile, so our realtor suggests we put in an offer of $305, assuming they’ll come back with a counteroffer. We already know we are ok with a $315k place, because including taxes, insurance, interest and PMI we can afford the $2,015/mo payment.

Everyone needs to be available to sign off on paperwork often during this part, so no one should plan a digital detox or be off the grid at this time.

10a – start working with your mortgage broker to make sure you have everything ready to go for them to write the loan. Once you put in an offer you’ll get your real numbers from the bank in terms of interest rate. You can still try to find a better rate but do it NOW to be respectful of all the work the broker is putting in.

Understand the following:

- unless you’re buying properties to rent, which is a business, only the person on the mortgage will get an extra tax reduction for their mortgage interest payments.

- the person taking on the mortgage is taking on a BIG responsibility and the broker and bankers are calling them all the time

10b – pay for an inspection on the house. Don’t cheap out on this potentially tens of thousands of dollars saving service. YES some things will come out of the inspection, and this is where your Agent is your ally so hopefully you’ve been delightful to them this whole time because now is when you want them to go to bat for you and negotiate – or be straight up about not worrying about certain things and running from others.

10c – make sure you each have a cash flow plan in place to start paying your part of the mortgage and house costs. Remember there’ll be a fair amount of upfront costs for moving, furnishing, and time off work to do these things. When you pay your closing costs, the first months’ mortgage payment is added in, so you’ll have a few more weeks than you think — but definitely be ready for the money to start flowing towards this. Agree together when you’ll each put money into your joint account, and how much.

10d – remember to celebrate, appreciate, and thank each other – no matter what happens!

Ready for more? Now that you’re in…

PART 2: Owning a house with other people

Managing house money, your future, and your friendships

Say you’ve acquired a home with other people – your partner(s), your best friend, your entire art collective… after you pause to breathe and celebrate this BIG accomplishment, your next step is to start to make transparent, inclusive, and intersectional plans to make sure you keep the place stocked and paid for by non-frustrated people who are minimally worried about their futures.

In short, you need to have a co-ownership plan. Here’s three things to consider when making it.

Keep the place stocked and paid for

You might have taken the advice above and gotten a joint account already, but if you haven’t, I can’t recommend it enough. Again, unless someone can’t be on an account, put everyone responsible for the place on the account, so each can deposit money and pay for things.

Note: if you have a business model / art residency / rental management situation going on here and you have an employee or a non-owner handling payments, decide if they need to be on the account or not – they may just need to be a signatory to deposit checks. As always, use your best judgement and err on the side of transparency 🙂

How much will everyone contribute?

Figuring out contribution is customizable, and where honesty and tracking are crucial.

Before you decide how you might split your contributions, you need a few pieces of information:

- How much does this all cost realistically, including mortgage, utilities, food, maintenance, creating an oh-shit fund, etc

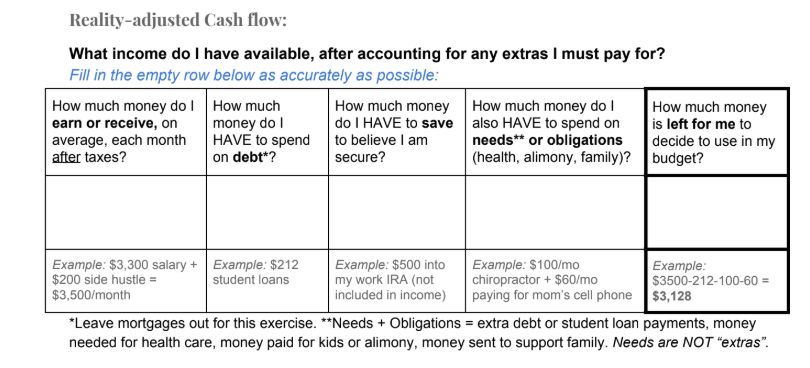

- What’s the resource reality of the people involved? As stated in my sliding scale, resources are about WAY more than income alone. Here’s a sample Reality-Adjusted calculator you could invite everyone to fill out, to account for their situations:

Now have a conversation. Perhaps your total cost is $3,000 and you have four people.

First: Is the split equal, in our example at $750 each or something else?

- Two of you have similar enough cash flow realities

- One of you makes about $10k more, but has the same outcome since they put most of their overage to retirement and student debt, given that they don’t have a family net

- One of you makes a lot less income than everyone else — but you all know from your experience buying together, it’s because that person has inherited wealth they count on, and which they kindly contributed extra from to the purchase in the first place

Next: If the split is uneven, do you track contributions to the equity (the value that accrues as you pay the mortgage) on the property equally or according to your split?

In our example above, I can imagine the group going with an equal split, even though they have unequal incomes — and I can also imagine an unequal split being considered equitable. At the end of the day, you’ll need to decide among yourselves what will feel right long term.

Then, agree when each of you will contribute your amount, and what will happen if you can’t. This may look like “We’ll each put a check into the account ourselves by the 28th of each month, we’ll tell everyone else if something is going on and we can’t do that, and we’ll identify if we need more money in the account to cover the upcoming mortgage payment.”

Finally, set a trigger event for when and if you’ll revisit this plan – if your taxes are reassessed and your costs go up? If one of you loses or gets a new job at a different income level? If someone’s situation changes and their life gets more/less expensive?

Read more about how to split and track shared costs among friends and beloveds here, and check out the Splitwise rent share calculator to learn what you might split if you used size / room niceness.

Keep the people involved non-frustrated

Define participation, responsibility, and expectations CLEARLY. Then, act accordingly.

Just like in a collective house you rent, no one wants to have the role of Dishes Mom or Rent/Mortgage Reminder Dad dumped on them.

For contributions, I suggested above making a clear agreement on when everyone puts a specific and transparent amount into a shared account. This is a good beginning. You can also make agreements on:

- Who checks the account to make sure payments aren’t bouncing

- Who makes sure the insurance / taxes are paid?

- Who liaises with contractors or bottom-lines it when things need to be fixed?

- Who maintains the grocery list and household items?

- Who sends out reminders for house meetings?

You’re grown enough to be legally bonded which means you’re definitely capable of telling people what you’ll do, when — and what you won’t do. For one group I worked with, this meant making a list of who bottom-lined which house chore: from checking the bank account to make sure the mortgage won’t bounce to handling green/garden things, let each other know who’s doing what so you can value each others’ physical and emotional labor like it deserves.

Finally, name your decision-making structure. Everyone-agrees consensus? Robert’s rules majority voting? What if someone isn’t present at a meeting where a decision that might impact them is made? What if someone decides never to come to meetings? In what scenario would someone not make a decision? Walk through the scenarios NOW so that you each know what to expect later.

Keep the future in mind

It is possible that one or more of the people involved may want to tap out before other(s) in the project. While I hope you discussed this before you bought, now — when you still like each other and everything is possible — is the time to put your plan in writing.

What could a future plan entail? Plan for the worst when you’re at your best.

I like to say to people who do this kind of business with me, “What do you want in place to protect you on the extremely slim chance that I decide to become a terrible person, or if I die and you want to ensure that a certain mean evangelical parent of mine has no claim to things we own together?” That tends to put it in perspective.

We all hope we’ll remain the generous best versions of ourselves and that our worst relatives will stay out of the picture, but that’s not realistic all of the time. Even realistically, when the moment comes that someone wants out, it’s not going to be simple. How about you answer the financial what-ifs ahead of time?

Firstly, getting Wills for all parties is a must. You own an asset together — make sure you have the paperwork (and the Deed) set up right in your State/Province so that when one of you dies, the asset (that is, the property) does what you expect and want.

This won’t be cheap as it’ll cost a few hundred bucks per Will, but it could save you WAY more than that in stress, taxes, and the avoidance of possible disaster later on. This is a DEFINITE get-a-lawyer situation.

Options for how you’d set up the Will include: your ownership passes to other owner(s), which is simplest but won’t pass your accrued value out of the people involved; or your ownership value in the asset passes on such that it can be bequeathed to whomever you decide — but be sure you have a plan in place so that whomever it passes to is someone you want to live there or there’s a way to get them the $$ value. Your lawyer can help you understand and create a plan.

Next, a basic exit strategy is crucial. The things people will wonder about include:

- Can I get bought out, and if so what would go into a buy-out?

- If I can get bought out, where will the money come from?

- If I can’t/won’t get bought out, what happens to my share later if and when the remaining owners sell?

- What would trigger a buy-out and what wouldn’t?

- How much would my buy-out be worth?

Calculating buy-out is no small matter for a few reasons:

- When you buy in, you’ll lose a chunk of money in closing costs

- As you pay the mortgage, a fraction of your payment goes towards the accruing value in the home, and you may want to track that fraction — and split it among the contributors

- As time goes on, the market resale value of the home may increase, and you may want to include that in the buy-out, or you may not; if the others are not selling the property, they are not realizing that economic gain, though they may if/when they sell.

Finally, can someone else enter the arrangement? How will they be looped into these agreements? What might buy-in look like for them? Adding them to the deed paperwork and getting them a Will might be a minimum requirement; asking them to “lose” the same initial amount other people did might be another.

Congrats, you’re a mindful co-owner!

Sure, sharing lives, resources, and space with other people isn’t simple. But given the social and economic benefits, many people choose to go this route. The outline above is what I’ve seen groups work through to positive effect, so get in there together. Or, reach out if you want support setting up these kinds of agreements!

Even though legal systems of ownership are set up for individuals and married couples, there still are many ways to set your ownership up if that’s not the setup you’re choosing. Here’s to all the kinds of families we make, and stability for each of them.

You also might like:

- the Money Tips to Buy a Home workshop

- this MEGA post on the Whys, Surprises and Ethics of buying a home

- the Guide to Talking About Money in a Relationship to get conversation tools and group budgeting suggestions.

Thanks to https://undraw.co for the cool open source images!