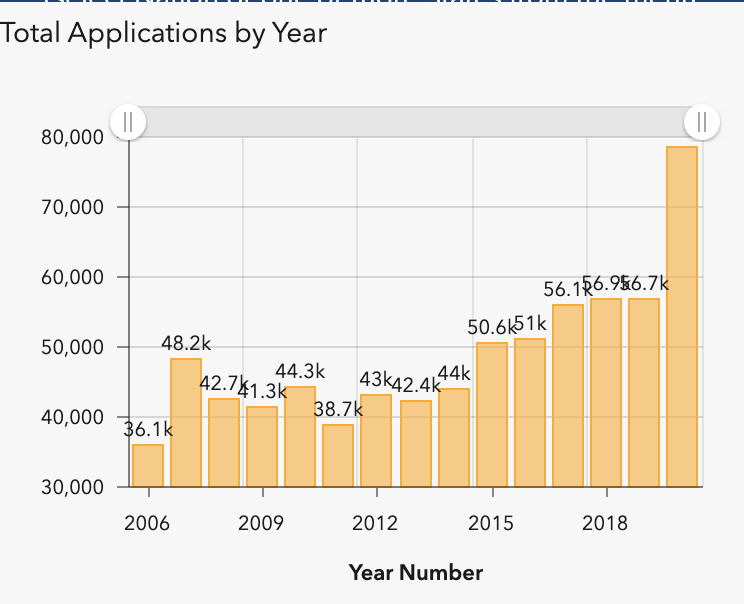

A 2020 phenomena is a spike in new businesses starting: EIN (business tax id numbers) applications are higher than they’ve been in 15 years.

So far it seems there’s two reasons: necessity and invention. Either business owners had to find a new way to make money after losing work due to COVID, or they saw a new opportunity due to COVID [here’s a few stories]. Either way – these new business owners are part of a launch wave. Welcome new friends and those of you considering joining these ranks!

I want business owners to succeed – and it’s hard! – So here’s my five Cs of success, some context, and the top five things to ask yourself before you set prices.

CONTEXT: DEFINING A SMALL BUSINESS

What’s called a small business – an enterprise run by one or a very few people and with revenues under $500k/year, is what banks refer to as “microbusinesses” – which make up the VAST majority of business enterprises.

Additionally, data are split between “employer” and “nonemployer” types of businesses.

- Do you run your own practice? You’re a nonemployer – and you make up 67% of all businesses in the US!

- Do you have under 5 employees? You make up 96% of employer businesses.

First, know your stage. Are you starting up, sustaining, or scaling? Each step has different needs.

| Startup | Sustain | Scale |

| Concept Charging | Cash Flow | Capital Collateral |

FIVE C’s FOR STARTING & SCALING

New businesses fail at an astounding rate: somewhere between 50% and 85% don’t make it past the 5 year mark.

TO START

- Concept & Charging – what am I going to offer, to whom, why do they want it, and how much money will I charge? Only you know what you want to share with the world – but the reality is that only by putting something out there can you see if the world wants that to be shared and how much various segments are interested to pay. You can fast-forward this process by testing pre-sales, one-off products and doing research – but nothing compares to getting out there, trying to sell, and seeing what you learn.

TOP FIVE THINGS TO ASK YOURSELF BEFORE YOU SET PRICES

- What are others in my field charging for this?

- How does what I’m charging relate to what others charge?

- If I charge this, how many services or sales do I need to to end up with the income I want?

- If I charge this, how long will it take me to do those services or sales?

- How will I feel about charging this much (or little)?

- Contacts – who you know and can work with, sell to, will recommend you is your most important asset when you’re starting out (and can’t afford massive marketing campaigns). Who will share your newsletter? Who will come visit your table at the outdoor market? These people are your champions – and if there are none, you’re going to have a harder time. Listen to what they tell you, and you will have an easier time.

TO SUSTAIN

- Cash Flow – making money in your business is kind of the point. You can’t “reinvest” it all, you have to make money and then take money as profit so you can…you know, pay rent and buy groceries or whatever you were planning on doing with the money. Set yourself up with a plan to charge, earn, and draw funds so your business is sustainable for you as it grows. (I have a pricing for sustainability template because this is so crucial for early-stage success.)

TO SCALE

- Capital – generating reserves (business-speak for ‘savings’) is a major next step. Not personally needing all the profits your business generates means you’re able to put funds to the next thing you want. At some point you may want to invest in your business, whether it’s renting a commercial space, leveling up your certifications to get larger contracts, hiring, buying yourself time to develop a product, or buying equipment. To do this, you need capital: that’s money honey. People get capital in the following ways:

- earned from your business to date and kept in reserves,

- saved from other endeavors (eg your other job),

- borrowed / gifted / invested from friends or family,

- Or, for a big expense, as a loan.

- Collateral – if you want a BIG loan, like to buy your commercial space or open a second location, you’re most likely to need a loan. It’s almost impossible to get business loans from banks when your business is new: if you’ve been around for less than 3 years and are seeking financing, you’ll want to go to the SBA for a loan. If you make it that far in (and many of you will!), then you’ll also need to demonstrate cask flow, some of your own capital, and collateral – a thing you can put up for the loan – in order to qualify for these big loans. That’s why, to scale, you need to have had strong cash flow and have been paying yourself.

**********************

Make Money & Do Good: A Social Impact Startup Guide

Quickly learn more about all these steps, including how to set your revenue and income needs, connect your concept to what you charge, and much more in this short but mighty business startup guide: