If your business — and by “business” I mean everything from a solo side hustle, full time business with employees, registered business or informal gigging self-employment — has seen loss of income due to COVID-19, look into government programs available for you.

This article is going to dig into one specific program in the US – so first, a resource for my Canadian readers!

- Department of Finance Canada – loans for businesses through your bank including a Small and Medium-sized Business Loan and Guarantee program + deferral of tax remittance for businesses and individuals — Business Development Canada made a more readable version ? of this info.

Onwards to the US content!

The short version: EIDL loan application pro-tips

If you’re going to apply for the US SBA’s EIDL loan:

- The online form is a super streamlined 3 pages, and you could do it on a smartphone

- Having your Feb 2019 – Jan 2020 accounting (gross revenue and COGS in particular) ready ahead of time is crucial

- You can call the SBA (at 1-800-659-2955), and a human will answer quickly to help you <3

The details: EIDL & PPP loan programs

First, there are two main federal programs available for small business owners (1-500 person businesses) who’s revenue, and therefore ability to sustain, has been impacted by COVID-19. Both of these are programs of the Small Business Administration (SBA).

- The Economic Injury Disaster Loans (and Loan Advance). You apply directly with the SBA. You can get up to $2M in loans and up to a $10k advance. The loan, if you qualify, is at a 3.75% interest rate and you can get up to 30 years to pay back any non-forgiven monies. The intention is to get working capital to impacted businesses ASAP, for “fixed debts, payroll, accounts payable, and other bills that could have been paid had the disaster not occurred.” (this is a darn comprehensive explainer).

- The Paycheck Protection Program (PPP), part of the CARES Act. You apply using a lending bank, and can get up to $10M, relative to the size of 2.5 months of your annual payroll. The loan is at a 1% interest rate, and any non-forgiven part is due in 2 years, though the intention of the program seems to be “use this to pay (and rehire!) employees and we’ll forgive everything you paid out to keep going and keep people employed.” Here’s a fact sheet for PPP borrowers from the US Treasury.

Portions of the loans under these programs are intended to be convertible to grants IF used for specific purposes, like paying: your employees (including yourself), mortgage interest, rent, and utilities.

I applied for the EIDL loan.

Here at Ride Free (aka RFFM LLC, the business entity), individual bookings are way down, and teaching contracts with organizations have dried up. I get it! And, I really want to keep paying the people Ride Free pays (my assistant! The cute local coworking space! And yes, myself!) I also wanted to see what the experience was like so I could tell you all about it. Here goes.

If you’re going to apply for the US SBA’s EIDL loan:

The online form is a super streamlined 3 pages, and you could do it on a smartphone

I was shocked by how simple this form was.

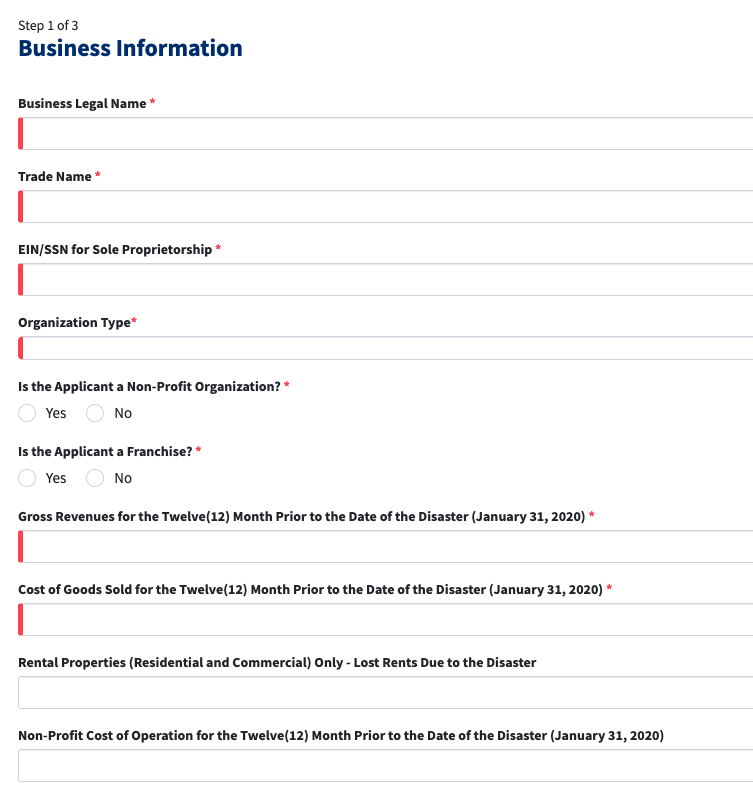

Page 1: Verify that you’re an eligible entity

Page 2: Specifics on the business entity, like EIN, address, Gross Revenues, COGS

Page 3: Specifics on the business owner(s), including SSN or TIN

Page 4: Affidavits, Banking info for the advance (if you qualify).

I was also shocked by both who could and couldn’t apply

Could: literally anyone who’s revenue was impacted, including part-time self-employed even if you don’t have a business entity, as long as you have the income and expenses documentation to back it up. NICE!!

Couldn’t:

Having your Feb 2019 – Jan 2020 accounting (gross revenue and COGS in particular) ready ahead of time is crucial

Page two of the form starts the “real” application.

There are two lines here you’ll need to have your accounting done in order to fill in:

- Gross Revenues for the Twelve(12) Month Prior to the Date of the Disaster (January 31, 2020)

- Cost of Goods Sold for the Twelve(12) Month Prior to the Date of the Disaster (January 31, 2020)

GROSS REVENUES

Note you aren’t going to give them what you put on your 2019 taxes, but if you have your 2019 taxes done you’ll likely have the data you need to recalculate.

This is how I calculated it:

Gross 2019 Revenue – January 2019 + January 2020 = Gross Revenues for the Twelve(12) Month Prior to the Date of the Disaster (January 31, 2020)

- I literally pulled Gross 2019 revenue from my 2019 accounting I got together for taxes

- Then I used my accounting software to calculate Jan 2019 total to subtract, and Jan 2020 total to add

- Finally I double checked in my payment processor and booking software to make sure I wasn’t missing anything

COST OF GOODS SOLD (COGS)

If your sales involve physical products, needed materials, and if you keep inventory, this is where your adherence to accounting will REALLY serve you, because you need to enter what it cost you to make your revenue.

Your 2019 taxes should have this information, so if you haven’t done your 2019 taxes this is your motivation and wake up call friends.

A few COGS how-to accounting resources: from WaveApps, QuickBooks, and the Balance, who write:

The basic COST OF GOODS SOLD (COGS) formula is:

- Beginning Inventory Costs (at the beginning of the year)

- Plus Additional Inventory Costs

- Minus Ending Inventory (at the end of the year)

- Equals Cost of Goods Sold

For example:

$14,000 cost of inventory at the beginning of the year

+ $8,000 of cost of inventory and other costs

– $10,000 ending inventory

= $12,000 cost of goods sold.

You can call the SBA, and a human will answer quickly to help you <3

Within 30 seconds of calling, at 9:30am ET, I was speaking to an informed person who answered my esoteric question. It was almost unbelievable, in this age of automation and endless phone trees, and apparently it’s the norm.

CALL THEM with your question, the SBA has people there to help and answer them for you: 1-800-659-2955. More details at the SBA site.

Policy Perspective

A final aside – these programs are intended to help keep small businesses, which are the heartbeat of our countries!, going – and creating these is doing the right thing. That said…

They’re going to exclude already marginalized people

For example, they’re not available to companies that create “purient” content which is silly because porn is a $12B industry.

Also if you’ve got a criminal record you might (unclear?) be unable to apply, which is going to have an outsized impact on race-biased criminalized populations, which is sociologist speak for that’s going to have a racist impact.

They’re debt

To be precise, any balance that’s not forgiven as a grant is debt, but still. This is a lot of debt for a lot of businesses to take on.

It’s not shocking that a system based on loaning money as debt, that’s essentially breaking right now BECAUSE so many people have debt obligations, came up with … more debt to help! I’m just not sure what next level of wake up call it will take to come up with a new solution (or a very old one, like jubilee), but for the moment, debt is what we have.

They’re also… a government handout!

So anyone who complains about “people who take handouts from the government / aren’t self-made / are morally inferior / etc” probably shouldn’t apply, on principle. Y’all just go pull yourself up by your bootstraps and get yourself out of this mess without these grant / loans.

The rest of us who run businesses, and who understand that it’s reasonable to contribute to public resources by paying taxes, also understand that it’s reasonable to expect to get public resources and services, like in a freak pandemic that causes our nation’s economy to literally grind to a halt.

Thanks for this!

My question is what counts as COGS for the EIDL. I understood from an SBA webinar that it could include payroll, rent, utilites, maybe some other costs to keep the business open (but I don’t know what counts.) This is different from what my accountant counts as COGS, which is basically just the cost of groceries we buy for our cafe.

I called the number and the representative could not give me a straight answer. He said: “Yes, include your rent etc.” Then: “Go with what your accountant says.” Those are two VERY different numbers!

Unfortunately, there’s no way I can give you better info than the SBA or your accountant. Those are the experts!