~video at the end of the post~

We need to talk about salaries.

Not just nonprofit salaries, but let’s start there.

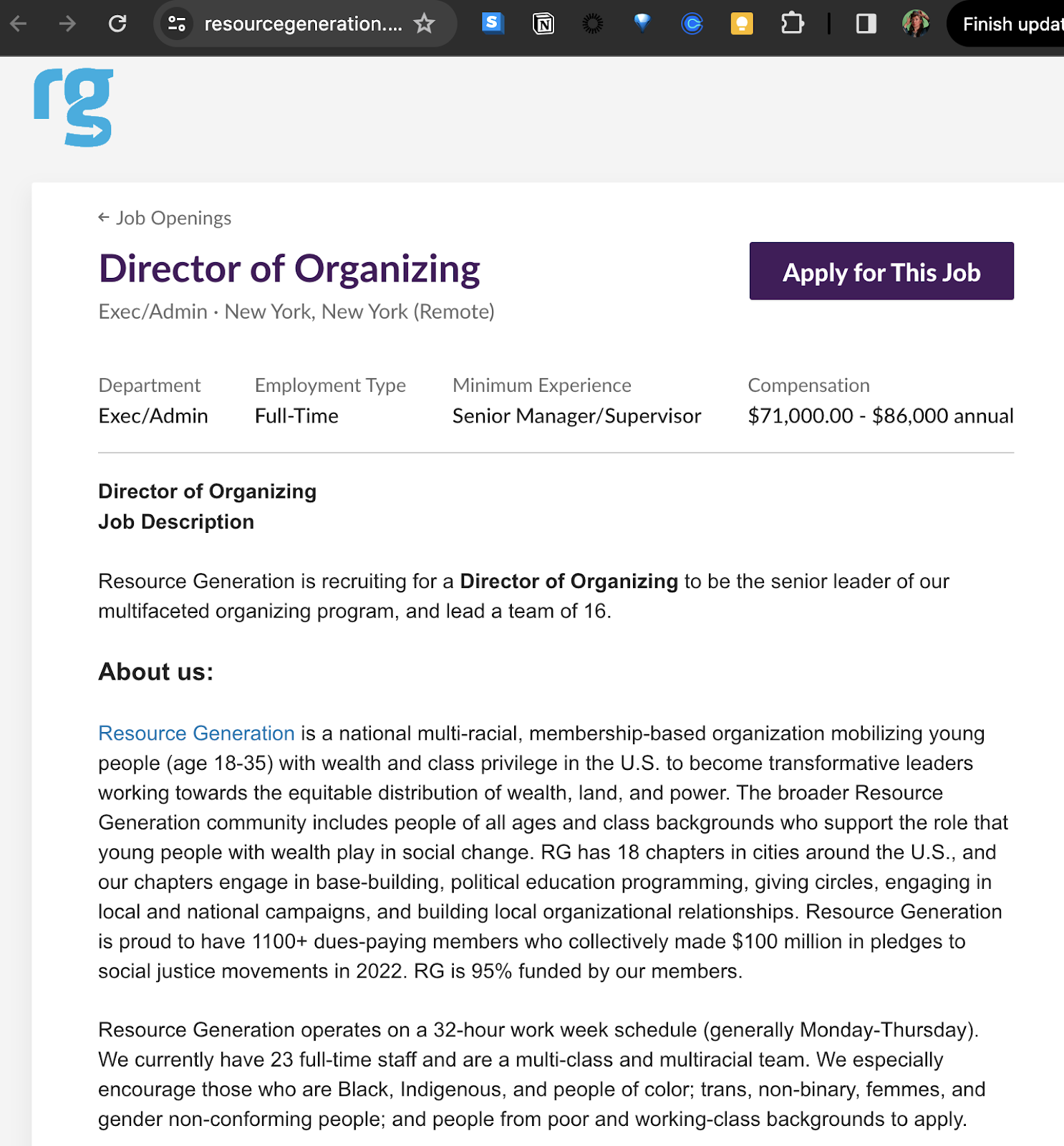

There’s currently a national nonprofit offering $71-86k for a director-level role [screenhshot below] – and they will pay the top of the range for people with 12+ years of experience who live in NYC or SF. The job is leading a team of 16 people plus doing organizing, and they are, of course, “especially encourag[ing] those who are Black, Indigenous, and people of color; trans, non-binary, femmes, and gender non-conforming people; and people from poor and working-class backgrounds to apply.”

We could stop right there with the giant scope of this role and how shockingly low the salary is for it, but: This organization does organizing with people who come from wealth, and much of the staff [and probably Board] are people with wealth. The job is to organize young people to redistribute their wealth. So, what they are asking for is for someone to do the job of working closely with people who have enough money they can give it away, at a salary that is going to force limiting financial choices on the person earning it – unless, of course, they have other income or wealth of their own to rely on.

But isn’t $80k great money? Some of you are surely asking. No, friend – it’s enough money to cover basics and then have prioritization decisions to make.

Let’s look at specifically HOW the salary they list – $71-86k – is set up to create an inequitable situation for someone from non-wealth to be hired, but first let’s understand why this salary might be tight and for whom.

How $80k a Year Is Not Enough

Is $80k “good money”? Arbitrarily, as compared to the $66k median income in the US, sure.

Wow that’s great! You might think. And it is a totally workable amount of money *if you don’t have other major costs or goals* – but if you’re also trying to fill in gaps that cost money on your own, it’s likely to be tight.

Let’s run a hypothetical single-person-with-no-family-money budget, which may be wildly unrelatable to you or might look a little familiar, but since I can’t write out 17 variations, please thought experiment with this:

$80k/yr is 6,600/mo before taxes. If you pay for $300/mo health insurance from your paycheck and put 5% into retirement ($333), that leaves $6,000 taxable – so that leaves you about $4,500 – maybe less if you’re in a higher tax city – after taxes, insurance, and a minimal retirement contribution:

First – your basics could take $2,500:

- Rent/mortgage – $1500 (or more)

- Food – $600 (or more)

- Gas/metrocard- $150

- Household stuff – $150

- Healthcare/gym – $100

Then there’s semiannual stuff – that averages $200/mo

- Car/stuff maintenance – $1000

- Gifts – $500

- Clothes – $1000

So you’ve spent $2700/mo to live …but what if you want to go out to eat, buy consumer stuff, have a pet, or go anywhere? Little niceties could quickly add up to $650+/mo

- Stuff – $100/mo (this is low but work with me)

- Travel – $2500/yr or $200/mo (could be less but usually folks want it to be more)

- Have a pet – food $50/mo

- Eating out and entertainment – +$300/mo (again this is low as compared to norms, but)

Now you’re at $3,350/mo to live relatively inexpensively but also travel, go out a little, get new clothes and stuff here and there. Those are your everyday life costs, bread and roses stuff – but what if you dare to want more, like a car or having an emergency cushion or general savings?

- Car down payment savings $500/mo (since your car payment+insurance might be in this range, or more!)

- Emergency savings – covering three months of basics in this case is $8100, if you wanted to save that over 2 years, that’s about $350/mo. If you have that cushion, you might keep saving for say a degree or a down payment, which if you’re trying to have $30k, will take 7 years at this savings rate.

Ok now you’ve used $4,200/mo to live, travel, create a cushion/save — hopefully you don’t have student loans, need dental work or more health care, have kids, or have people in your life who need money. Let’s think about situational needs:

- House maintenance – $1000-5000/yr

- Have kids +$$$??

- Have kids in daycare – $12,000-24,000/yr

- Have a high cost/uncovered health needs – $$??

- Have family who needs assistance – $$??

- Student loans or old debt -$$??

- Want to pay for gender affirming care – $$??

Here’s where it gets sticky: saving for your emergency or car is where most people would cut, then start reducing going out, clothes etc. This is how people end up with credit card debt (which we also didn’t include a payment for). Hypothetically there’s $300/mo left to cover any of this…or $650/mo if you abandon saving for an emergency. Good luck, especially if you have kids!!

This is where the tough choices come in – your basics might be covered but the other things are all a swirl of competing priorities and it’s a hellscape, also known as the collapse of the middle class

So: is $80k a lot. Yes, and filling in non-monthly financial needs, if you have them, gets expensive fast. So if you feel like others are making it work on whatever lower salary, they may simply not be, or they might have other resources to make it possible. It’s when people without these compare themselves to people with, without realizing this is happening, that we feel like something is wrong with us for not being able to make it work.

THIS SPECIFIC JOB LISTING

In the context of the specific job we are investigating, it’s highly possible that other staff, with wealth might have been given cash reserves, or have had a family member buy them a home or pay for their kids’ needs.

On their own these are not bad things to have!! But these differences in fundamental needs to cover are why this salary is going to set up a hire from a financially-marginalized background to be choosing between say, saving for a personal financial goal, clothes/food/trips/housing as nice as the ones the people they are trying to organize have, and do the kind of catch-up/hole-filling saving that people from financially marginalized backgrounds have to do.

The job listing specifically encourages “those who are Black, Indigenous, and people of color; trans, non-binary, femmes, and gender non-conforming people; and people from poor and working-class backgrounds to apply,” so let’s be clear: If your hire isn’t coming to the table with wealth, this salary is going to put them in a disadvantaged situation as compared to the people they are organizing.

What if the ideal candidate is single or COVID-cautious and doesn’t share rent? What if that person has to pay for childcare, expensive health needs, has student loans, needs to save money for their retirement if they have no inheritance to cover their future, needs to give money to family, is saving for gender-affirming healthcare, or is seeking to get out of debt …

As I broke it down above, there is sadly not a lot of money at $80k to cover all the kinds of accumulated life needs that people without wealth have AND regular life costs AND have money left over for financial goals [adoption, buy an apartment/house, take a sabbatical] etc AND live a little. It can feel really gaslighting and like an individual failure, to feel tight on $80k, especially if you have friends or colleagues who seem to make it work, when what’s really happening is that coming from different lived experiences and backgrounds, you need different amounts of money to be on the same playing field.

There is also a real risk of exploiting someone from a lower-income background who does not realize that a salary for this kind of role should be higher, because they don’t come from higher-earning communities. If you think $80k is a lot and you see your coworkers making it work and you don’t realize they have had help, you could feel like a failure when it’s not you.

Same salary, different kinds of needs = not equitable.

With RG specifically, why not leverage a small fraction of the resources being moved to create a thriving wages situation for staff — or just be clear that the intention is to hire someone who doesn’t need to earn a wage to cover their needs. I can imagine there might be reluctance on the part of staff who do have wealth, to set high salaries for themselves that they don’t perceive they need. Maybe RG needs a dual track salary scale: do you have a trust over $xxxk? This, low-paying track. Do you not have access to wealth? This, other market-rate track. There are ways to solve this that don’t create this situation.

IMHO this salary should have a 1 in front of it [eg $171k-181k] especially if you’re hoping to hire a senior person in NY/SF, to be inclusive for people from lower-income experiences – and to be at market rate. Allied Media Projects’s Director roles pay $129-162 mapped to midwest market norms, and they also have a 4-day work week.

I have to be honest, this makes my blood pressure rise and is a prime example of everything that could go wrong with nonprofits: mission above financial sustainability with classist rose-colored glasses. Given that this organization literally and specifically has access to money and an economic justice intention, I feel so disappointed in RG seeing this salary [not to mention the huge role scope].

As a queer femme who comes from a poor/working class background, I hope this POV gets shared with decision-makers at RG. I would be happy to connect them with the people who AMP worked with to do their equitable salary study, in the hopes of doing better and creating an organization that can equitably hire the people it seems to want to.

So, now what?

Let’s break this silence: talk about what you earn with others! Ask other people what THEY earn. Look at job postings with salary listings, or at salary databases [I like this one]. And stay tuned for a project I’m working on that deals with jobs, money, and finding work you want that also pays enough, coming out in March <3